The cash flow statement is one of the essential financial tools that managers and financial analysts rely on to understand and evaluate a company’s performance and make critical financial decisions. Understanding how cash flows in and out of a company is crucial to ensuring the sustainability of business operations and achieving financial growth. This article aims to provide a comprehensive overview of the cash flow statement and its importance, as well as explaining the key steps in preparing it and how to analyze it effectively .

What is a cash flow statement?

The cash flow statement is an accurate financial report that shows the movement of cash in and out of a particular company during a specific period of time, stemming from the economic, operational, financing, and investment activities undertaken by the institution. This statement highlights all financial transfers and expenses incurred by management to implement and complete its commercial and investment activities .

This financial report is an essential tool for understanding and analyzing an organization’s financial performance. It works in conjunction with other financial statements, such as the balance sheet and the income and loss statement. Every organization must prepare these three statements in accordance with a set of globally recognized accounting standards. These statements enable management to forecast the organization’s cash position and develop appropriate short-term economic plans. Consequently, management can make sound decisions based on a comprehensive analysis of economic activity .

Components of the cash flow statement

The cash flow statement is one of the key financial tools that helps companies understand the movement of cash within the organization. It consists of three basic components: cash flows from operating activities, investing activities, and financing activities. Let’s take a deeper look at each of these components to understand how they impact a company’s financial performance .

1- Operational activities

This component of the cash flow statement is called cash flow from operating activities. It relates to cash transfers arising from the company’s day-to-day activities. The cash flow from these activities is an important indicator of a company’s ability to generate cash from its core operating activities. These activities include supplier payments, customer receipts , tax payments, rent costs, and employee wages .

2- Investment activities

The statement of cash flows from investing activities highlights the cash transfers associated with investments in fixed and non-fixed assets. It records the costs of purchasing and selling assets such as buildings, equipment, and land. It allows a company to understand how it is investing funds in the property to achieve the desired return .

3- Financing activities

The statement of cash flows from financing activities relates to how a company finances its operations and growth. It records cash transfers related to debt and equity, such as loan repayments, dividend distributions, and capital raising. It provides investors and shareholders with a deeper understanding of how a company manages to finance its operations and the impact of cash generated from these activities .

We can say that the components of the cash flow statement are essential elements for understanding how a company generates and uses cash. They help guide critical financial decisions to ensure the successful continuity of business activity. Net cash flow is the result of a combination of these components and is an effective indicator of a company’s financial health and its ability to grow and develop .

What is net cash flow?

Net cash flow is defined as the difference between the cash paid out and the cash received by an organization during a specific period of time. This net cash flow is calculated monthly and reflects the amount of money the organization needs to finance its operations, whether for expansion, research and development, purchasing new equipment, or even to pay off outstanding debts. This cash flow may also include short-term investments that require cash transfers .

As for the equation for calculating net cash flow, we can express it as follows :

- Net cash flow = Cash flow from operating activities + Cash flow from investing activities + Cash flow from financing activities .

When the result of this equation is positive, it reflects a strength of the institution, while a negative result warns of the risk of bankruptcy if it continues for a long period .

Although achieving negative net cash flow is worrisome, it doesn’t necessarily mean the organization is in danger. Rather, this decline could be due to the organization’s investments in new expansions or equipment upgrades, which could lead to positive results in the future. Therefore, analyzing the causes of this decline is essential to determining the correct actions and dealing with the situation appropriately .

What is the purpose of a cash flow statement?

Cash flow statements are a vital tool in the field of economics for companies and institutions, as they provide a comprehensive picture of the impact of various economic activities on the cash available to them during a specific period of time. These statements aim to guide financial management and decision-makers in companies to make sound decisions to ensure the continuation of operations effectively and the achievement of specific financial goals. Below we review the most important objectives of the cash flow statement :

1- Analyzing and tracking outgoing cash flows

The cash flow statement provides an accurate overview of the various expenses arising from the various activities of the business, such as paying off debts, purchasing inventory, and operating costs. This, in turn, helps in monitoring how cash is spent and controlling it effectively .

2- Directing financial strategies

Cash flow statements help plan for a company’s future financial needs, whether for expansion, operational improvement, or to cover future financial obligations. This helps avoid financial risks and ensure business continuity .

3- Verify the accuracy of cash flow forecasts.

The cash flow statement verifies the accuracy of the cash flow budget prepared for the company. If expectations match reality, this reflects the soundness and stability of the budget. If there is a positive difference, this means that expectations have been exceeded and a cash surplus has been achieved .

4- Crisis planning and effective financial decision making

How to prepare a cash flow statement

Preparing a cash flow statement is vital for every organization seeking to understand and manage cash flow in its financial activities. In this guide, we will review nine key steps for preparing this statement efficiently and accurately .

1- Time frame

Before starting to prepare the cash flow statement, we must determine the appropriate time period that the statement will cover, based on the nature of the business and the needs of the facility. This determination also includes studying the nature of the facility’s cash transactions during that period .

2- Creating the integrated context

The cash flow statement measures the income and expenditure of an entity. Cash flow data is detailed in the balance sheet and income statement. The arrangement of financial statements aims to integrate financial data to ensure consistency and balance between assets, liabilities, and equity. Therefore, it is recommended to carefully review and audit this data to ensure the accuracy of the net profit equation and to ensure consistency between the numbers entered and the final result in the statement of financial position .

3- Opening balance

This step involves determining the organization’s opening cash balance for the period covered by the cash statement. This balance is of utmost importance, especially when using the indirect method of calculating cash flow from operating activities. However, this step is not necessary when using the direct method . The cash flow statement serves as an important analytical tool for making sound financial decisions within the organization. It provides data that helps set priorities and effectively manage financial crises, in addition to improving profitability and increasing the efficiency of the use of financial resources .

4- Calculating cash flow from operating activities

This stage is one of the most important steps, as it highlights the amount of cash generated as a result of the organization’s operating activities. This flow can be calculated directly or indirectly. Choosing the appropriate method for preparing the cash flow statement depends on several factors, such as the size of the organization and the resources available for preparing the financial statements. During this stage, focus must be placed on the objective of applying the chosen method to the operating activities involved in the cash flow statement .

5- Collecting expenses and non-cash transactions

At this stage, the recording of missing non-cash transactions in the income statement and other financial records should be verified. It also requires updating any adjustments to these transactions, such as depreciation costs for fixed assets, bad debts, and losses resulting from changes in the value of assets. In addition, the impact of changes in exchange rates, interest rates, and foreign currencies should be monitored, as these can directly affect the cash value of transactions .

6- Cash flow analysis

This stage of the cash flow statement process requires analyzing all cash activities. The analysis begins by tracking operating activities to measure revenues, expenses, and changes in accounts payable and receivable. Investing activities, such as the purchase and sale of assets and investments in securities, bonds, and other assets, are then analyzed. Finally, cash flows from financing activities, such as loans, dividends, and financing transactions related to the purchase or sale of stocks, are tracked .

7- Calculating the closing balance

This paragraph refers to a fundamental step in the process of preparing a cash flow statement. After completing all the previous stages in the process, such as determining the time period, compiling the financial data, and calculating the cash flows from various activities, comes the turn to calculate the closing balance. This closing balance is the cash available at the end of the specified period, and represents the remaining cash after conducting all the various financial transactions during the specified period .

These operations may include paying bills, receiving payments from customers, making investments, repaying loans, and other activities that affect the amount of cash available to the organization. If the process is carried out correctly, the final cash balance is obtained, which is presented in the cash flow statement as the end point for the specified period .

8- Calculating the difference between the opening and closing balances

The accuracy of all accounting values that constitute the opening and closing balances of the recorded transaction accounts must be verified and documented with documentary evidence. The figures must be free of errors and accounting errors, whether intentional or unintentional. The differences between the opening and closing balance accounts that form the cash flow schedule must then be monitored and recorded .

9- Preparing a cash flow schedule

Preparing a cash flow schedule requires dividing it into three sections :

- Cash flows from operating activities .

- Cash flows from investing activities .

- Cash flows from financing activities .

Each activity in the table is then detailed horizontally to record its accounting items, followed by performing the calculations for the items in each activity to arrive at the final balance. Finally, the final balances of the three activities are combined to obtain the net cash flows. This list can be disclosed to the relevant parties after verifying its accuracy, as it is an essential part of the financial reports of the applicable entity .

When do I prepare a cash flow statement?

The cash flow statement represents a fundamental step in the financial reporting process for organizations. This statement comes after the preparation of basic financial statements such as the statement of financial position and the statement of profit and loss. Typically, the cash flow statement comes third in the order of financial statements, preceded by the statement of financial position and the statement of profit and loss .

Preparing a cash flow statement is a precise and systematic process, where all financial transactions that affect an organization’s cash flow over a specific period of time are analyzed and systematically presented in a detailed, organized list. This list focuses on actual cash flow and clarifies its sources and uses. This goal is to demonstrate the organization’s ability to manage cash and ensure its sustainability in daily operations and future investment projects .

The order and timing of financial statements vary depending on the requirements of each organization. However, the cash flow statement is usually prepared periodically, whether monthly, quarterly, or annually. This provides a continuous and accurate view of cash flow and its uses, which contributes to making sound financial decisions and achieving the organization’s goals efficiently and effectively .

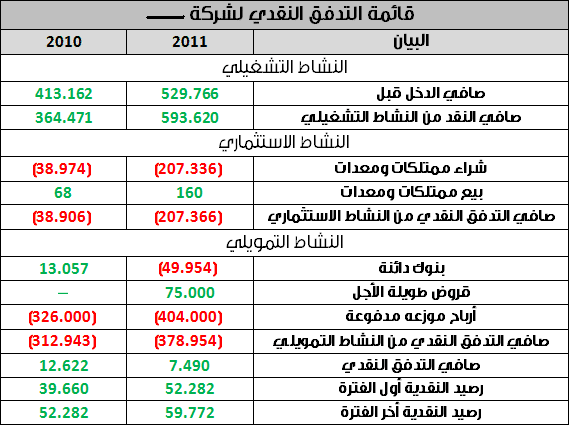

Cash flow statement format

{kind=link}

Direct cash flow method

The direct method for calculating cash flows relies on adding up all transactions that require the payment or receipt of cash during the specified time period covered by the cash disbursements statement. This is done by calculating all amounts collected in cash through operating activities and then subtracting all expenses paid for these activities. This method uses specific equations :

1- Cash received from customers

This equation calculates cash collected from customers by adding net sales and the decrease in accounts receivable and subtracting the increase in accounts receivable and accounts payable .

2- Cash received from various sources

This equation calculates the total cash received from other sources such as interest or dividends. The interest or dividend income and the decrease in unearned accrued revenue are added together and the increase in unearned accrued revenue is subtracted .

3- Cash paid to the supplier

Cash paid to suppliers is calculated using two equations: the first calculates the value of purchases, and the second calculates cash paid to suppliers, including increases and decreases in accounts payable .

4- Cash paid on expenses

This equation calculates cash paid on expenses by adding up expenses during the period and their adjustments, plus increases and decreases in prepaid and accrued expenses .

Indirect cash flows

The indirect method of calculating cash flows begins by calculating net profit before adding taxes, accrued interest, depreciation of tangible assets, and amounts paid to suppliers, allocating any shortages in merchandise and reductions and increases in advance payments from receivables. This is done after deducting what has been collected from customers and increases in merchandise .

To calculate cash flows using the indirect method, the following equation is used :

Cash flow from operating activities = Net profit + Non-cash expenses + Cash from operations + Decrease in accounts receivable + Decrease in merchandise inventory + Decrease in prepayments + Increase in accounts payable + Increase in accrued expenses – Increase in accounts receivable – Increase in merchandise inventory – Increase in prepayments – Decrease in merchandise inventory – Decrease in accrued expenses + Income tax paid .

Although the direct method is easier to understand, it can take longer as every transaction during the period must be accounted for. Therefore, many organizations prefer to use the indirect method to calculate cash flows .

In conclusion, both methods – direct and indirect – provide three key financial metrics that are pivotal in cash flow analysis. These metrics include: the percentage change in net cash flow, which reflects the organization’s internal cash flows; the cash flow from operating activities ratio, which reflects the ability to generate cash from the organization’s core activities; and the cash flow from investing and financing transactions ratio, which demonstrates how funds are managed and directed in investing and financing activities .

Leave a Reply